Table of Contents

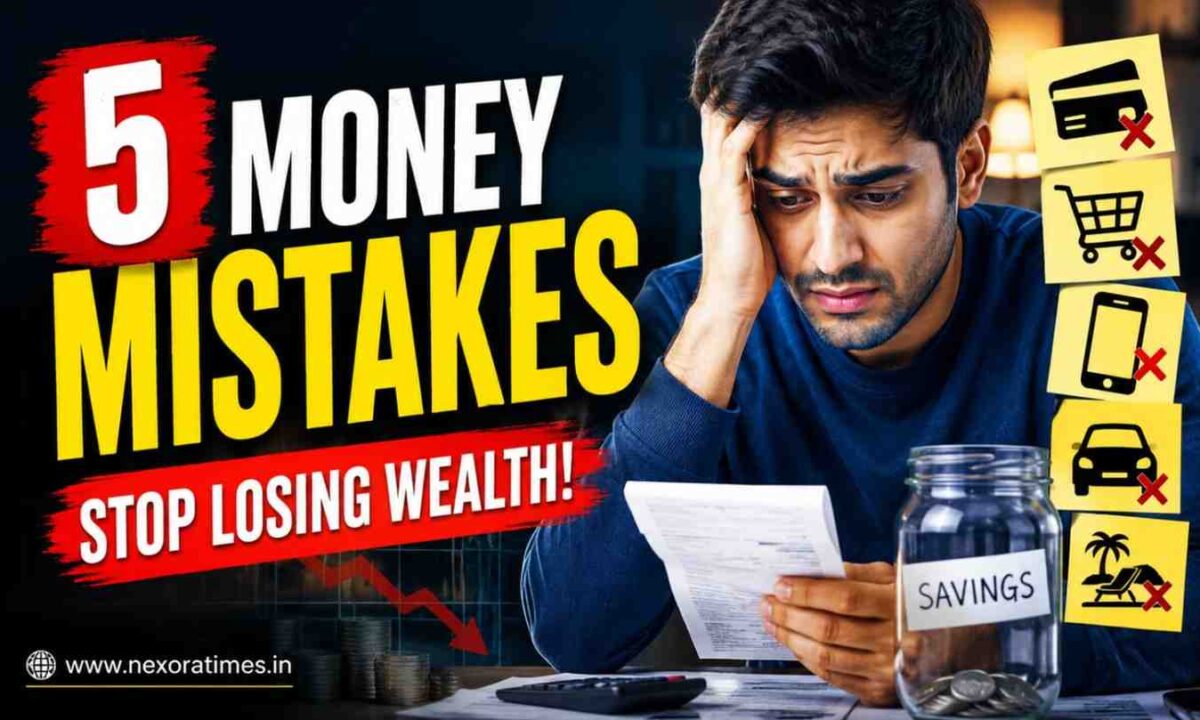

Millions Are Earning More in 2026, But These 5 Money Habits Still Hurt Wealth

For many Indians, 2026 has been a year of rising salaries, expanding investment options, and easier access to credit than ever before. Yet financial experts say one uncomfortable reality remains unchanged: earning more money doesn’t automatically create wealth.

Across social media, finance communities, and investment forums, a growing conversation is emerging around why so many people still struggle to build long-term financial security despite higher incomes. The answer often isn’t a lack of opportunity. It’s a handful of money habits that quietly drain wealth over time.

What makes these mistakes dangerous is that they rarely feel like mistakes in the moment. They often appear normal, practical, or even rewarding. But years later, the financial consequences become difficult to ignore.

Lifestyle Inflation Is Growing Faster Than Income

One of the biggest personal finance trends of 2026 is lifestyle inflation.

Many professionals receive salary hikes, bonuses, or freelance income increases. Instead of directing the extra money toward investments or savings, a large portion often goes toward lifestyle upgrades.

Common examples include:

- Upgrading smartphones every year

- Taking frequent financed vacations

- Increasing EMI commitments

- Moving to more expensive rentals

- Spending heavily on premium subscriptions

The hidden problem is that expenses rise permanently while income growth remains uncertain.A salary increase should ideally improve future financial security. However, many households unknowingly convert higher earnings into higher monthly obligations.

Depending Too Much on Credit and Buy Now, Pay Later Services

Instant credit has become deeply integrated into India’s digital economy.From shopping apps to travel platforms, consumers can now split payments into easy installments with just a few clicks.

The convenience is undeniable. However, finance experts warn that many consumers underestimate the psychological impact of easy borrowing.

Warning signs include:

- Multiple active EMIs

- Frequent use of Buy Now, Pay Later options

- Credit card bills carried forward every month

- Borrowing for discretionary purchases

The real issue isn’t debt itself. Responsible borrowing can be useful. The concern begins when future income is repeatedly used to fund present consumption.

A growing number of young professionals are discovering that small monthly payments can quietly accumulate into a major financial burden.

Investing Without Understanding Risk

The investing culture in India has expanded dramatically.Stock market participation, mutual fund SIPs, ETFs, digital gold, and global investment discussions have become mainstream. While this is largely positive, another trend has emerged alongside it.

Many investors are chasing returns without fully understanding risk.

Popular mistakes include:

- Investing based solely on social media tips

- Following influencers without research

- Buying trending stocks because everyone else is buying

- Expecting unrealistic returns in short periods

The biggest losses often occur when investors enter markets during periods of excitement and exit during periods of fear.

Successful investing is usually less about finding the next big winner and more about maintaining discipline during uncertainty.Long-term wealth creation often appears boring compared to viral investment stories, but historically, consistency has proven far more powerful.

Ignoring Emergency Funds Because Investments Look More Attractive

One surprising trend in 2026 is that many people are investing before building an adequate emergency fund.This happens because investing feels productive. Keeping money in a savings account often feels like missed opportunity.

Job losses, medical situations, family obligations, business disruptions, and unexpected expenses can quickly force people to liquidate investments at the worst possible time.

A strong emergency fund can help:

- Avoid high-interest debt

- Reduce financial stress

- Protect long-term investments

- Improve financial flexibility

Many financial planners continue to recommend maintaining several months of essential expenses in easily accessible funds.Despite this advice being widely available, emergency preparedness remains one of the most neglected areas of personal finance.

Delaying Retirement Planning Because It Feels Far Away

Retirement planning remains one of the most postponed financial goals among Indians.For someone in their twenties or thirties, retirement feels distant compared to immediate priorities such as housing, travel, family responsibilities, or career growth.

Why delay becomes expensive

Even a few years of postponement can significantly reduce the benefits of long-term compounding.Many people believe they can “start later when income is higher”. However, waiting often requires much larger contributions in the future to achieve the same retirement target.

The conversation around retirement in 2026 is shifting. More young professionals are recognizing that financial independence isn’t only about old age—it’s also about creating flexibility and freedom earlier in life.

FAQs

- What is the biggest money mistake Indians make in 2026?

Lifestyle inflation remains one of the most common mistakes. Higher income often leads to higher spending instead of increased savings and investments.

- Is Buy Now, Pay Later bad for personal finance?

Not necessarily. It can be useful when used responsibly, but excessive reliance may create debt and cash-flow problems.

- How much emergency fund should a person have?

Many financial planners suggest keeping at least 3–6 months of essential expenses in accessible savings.

- Why is retirement planning important in your 20s and 30s?

Starting early allows investments to benefit from long-term compounding, reducing the amount needed later.

- Can investing alone make someone financially secure?

Investing is important, but it works best alongside budgeting, emergency planning, debt management, and long-term financial discipline.

Conclusion

India’s financial landscape is evolving rapidly, but the biggest wealth-building lessons remain timeless. The challenge in 2026 isn’t a lack of information—it’s turning that information into consistent action.

The people who avoid these common money mistakes today may find themselves significantly ahead a decade from now. As conversations around financial independence continue to grow, one question remains worth asking.

Follow Us: Instagram

For more information: Financial Market Trends in India 2026: Big Shifts Revealed

Adani Total Gas Share Price Today: Big Update, Trend Analysis & 2026 Outlook Revealed

{kind=link}